Best Credit Cards in April 2024

14 Best Rewards Credit Cards in April 2024

NEW

Introducing LendingTree Spring

Personal Loans

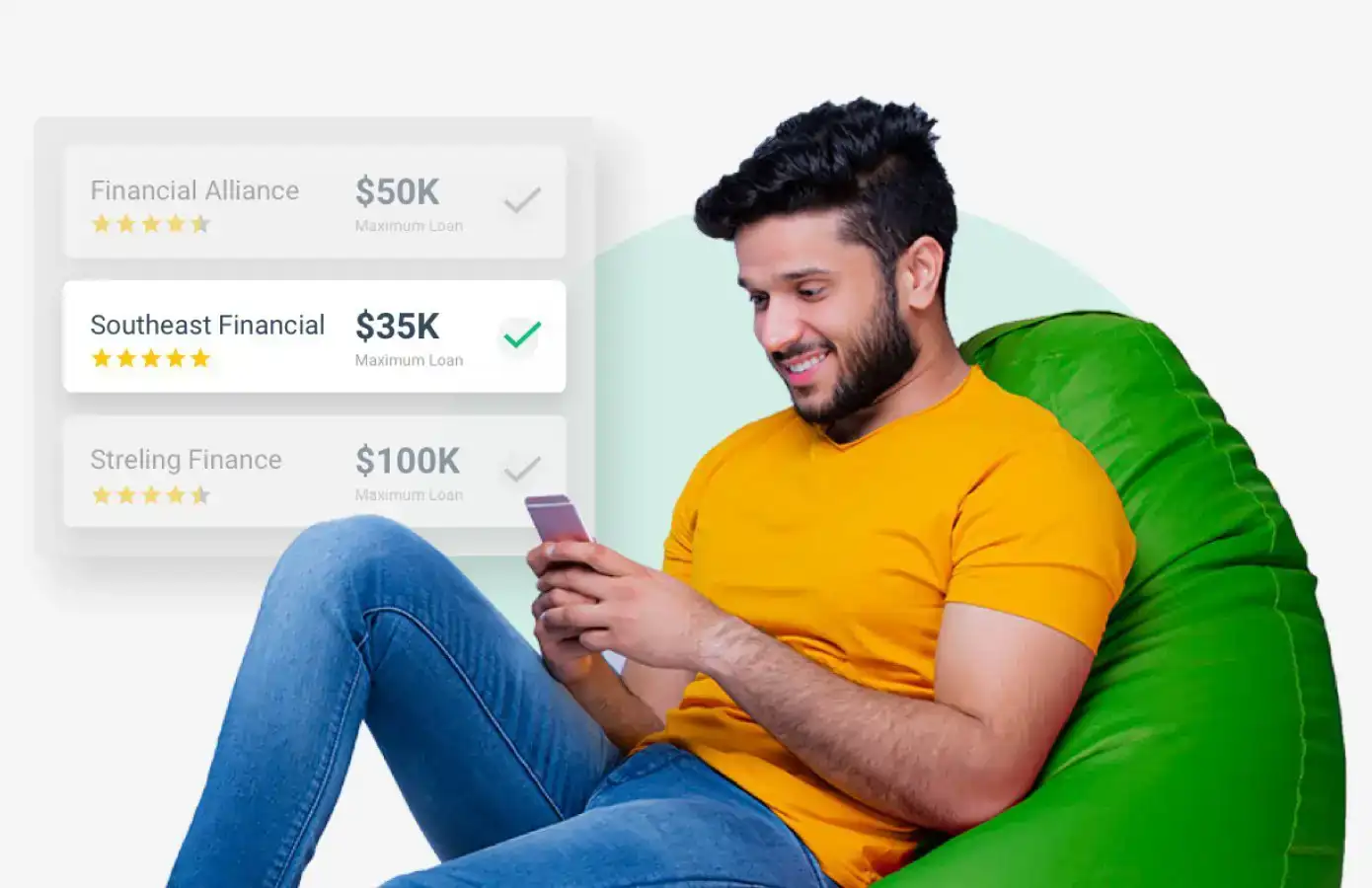

Find the right personal loan rate for you

Need to consolidate debt or make a large purchase? We bring the lenders to you so you can shop and compare personal loan offers in minutes.

Privacy Secured | Advertising Disclosures

Home Equity

Put your home’s equity to use

With home values higher than ever, now’s the time to make the most of your equity. Compare offers in minutes.

Privacy Secured | Advertising Disclosures

Home Purchase

Compare top mortgage lenders

Get multiple lenders to compete for your business and see how much you could save. It pays to compare your options — literally.

Privacy Secured | Advertising Disclosures

Credit Cards

Shop and compare credit cards

From earning rewards to transferring a balance, find the right credit card to help you score everyday wins.

Privacy Secured | Advertising Disclosures

Insurance

Find the best insurance rates for you

Compare top insurance companies and get affordable, customized coverage for your car, home and more.

Privacy Secured | Advertising Disclosures

Business Loans

Shop and compare business loans

Our network of lenders will compete for your business, so you can get the funding you need for yours.

Privacy Secured | Advertising Disclosures

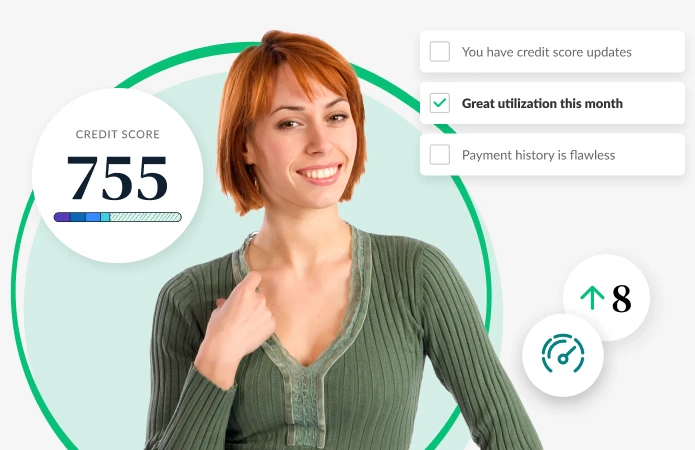

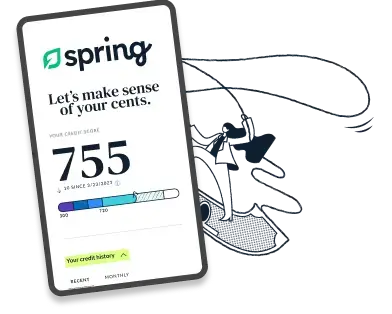

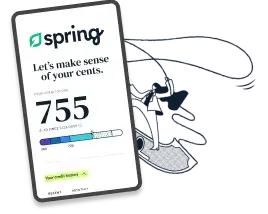

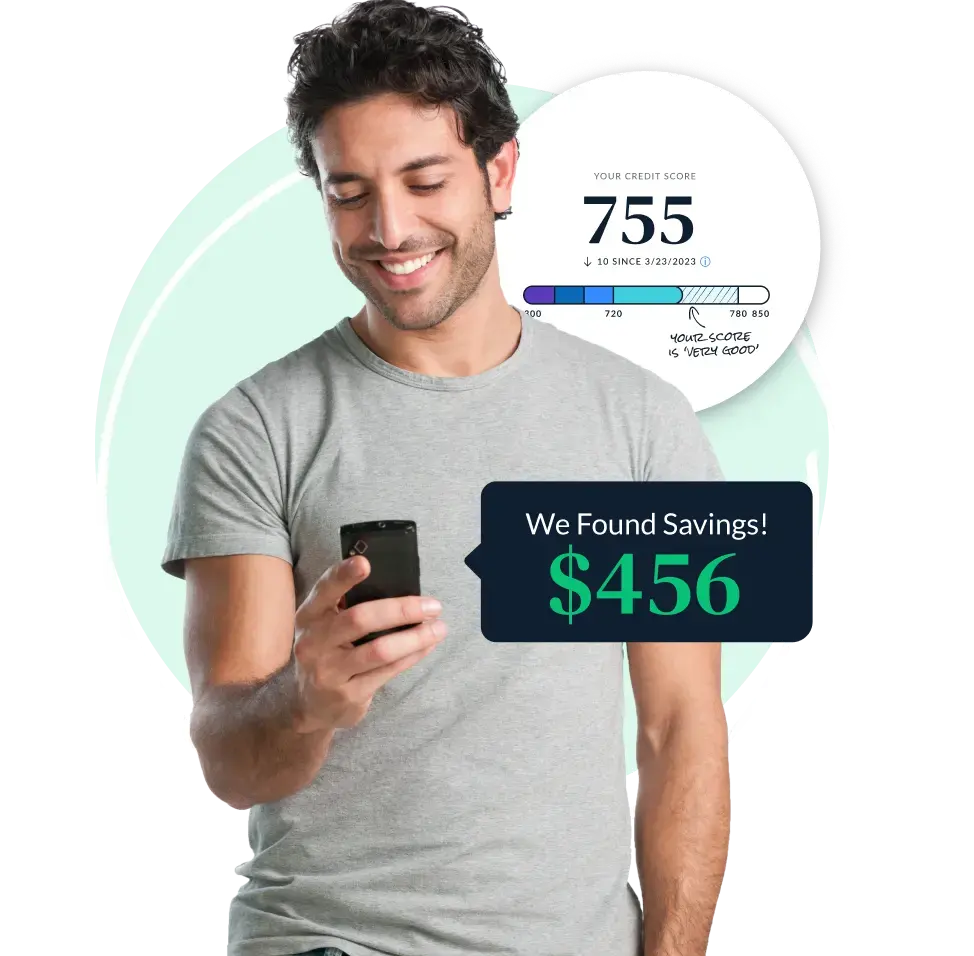

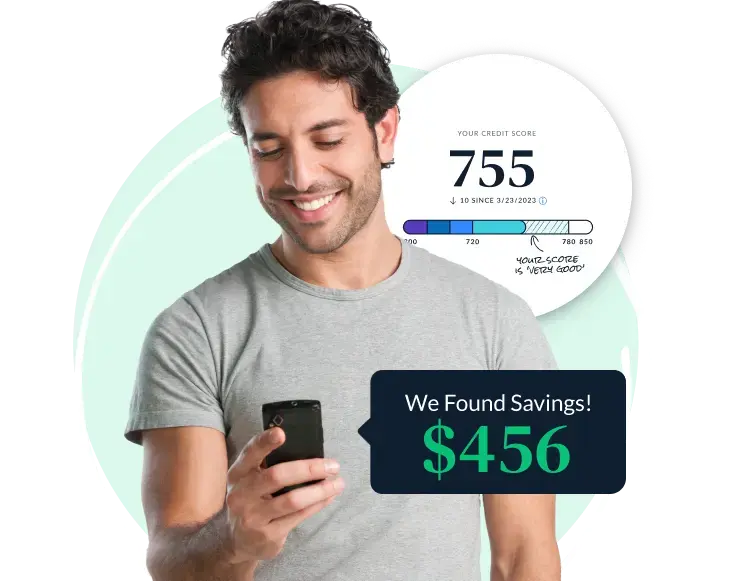

LendingTree Spring

Where smart habits take root

Track your credit score, get personalized financial recommendations, and grow your credit health — all in LendingTree Spring. It’s free and available now!

Privacy Secured | Advertising Disclosures

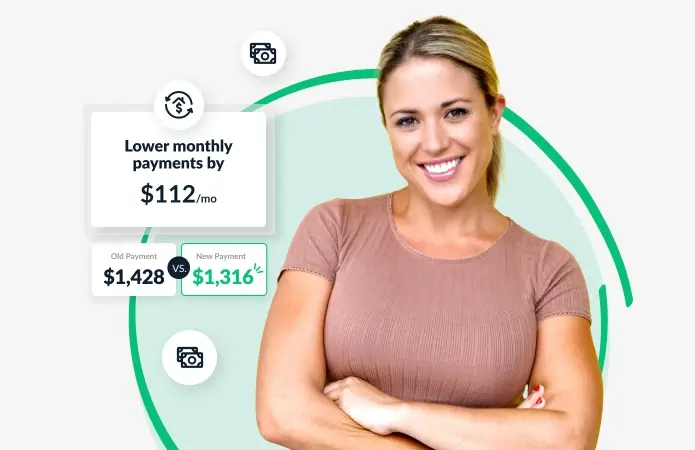

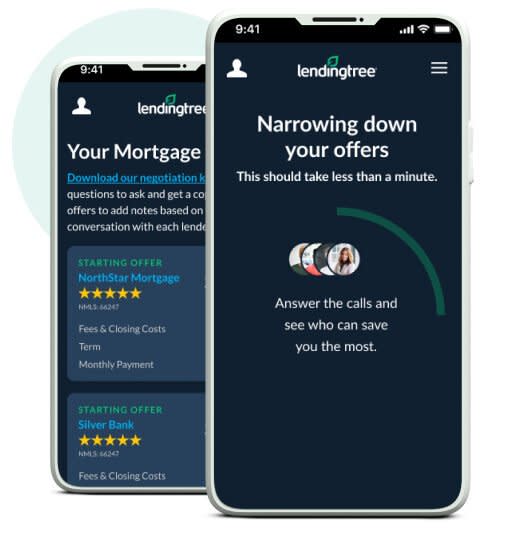

Home Refinance

Compare mortgage refinance offers

Get personalized refinance offers from multiple lenders in minutes and see how much you could save on your mortgage.

Privacy Secured | Advertising Disclosures

Debt Relief

Compare debt relief options

It’s never too late to find relief. Stop juggling bills and resolve your debt with one simple monthly payment.

Privacy Secured | Advertising Disclosures

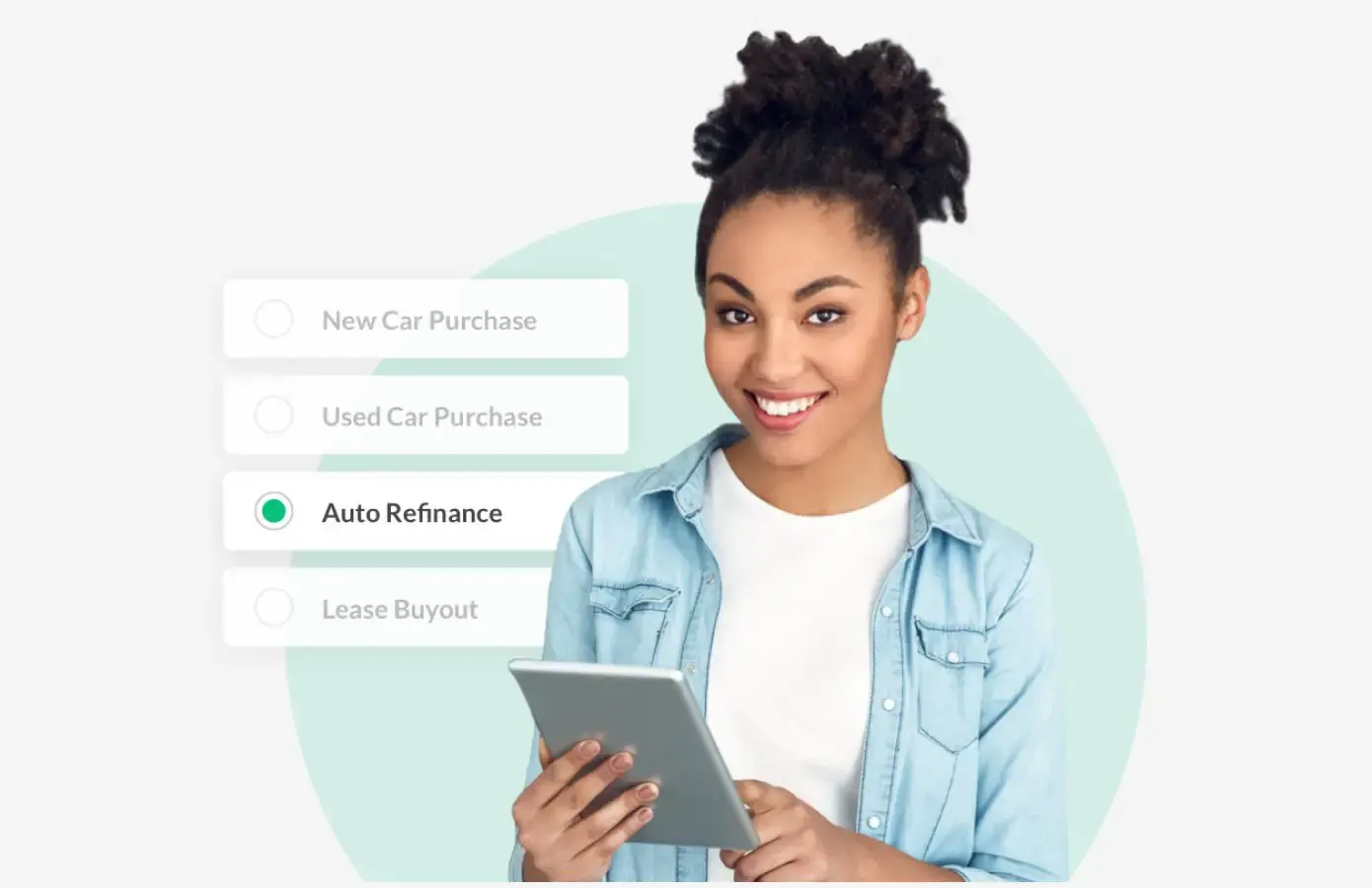

Auto Loans

Discover the right auto loan for you

Take home the car you love. Compare auto loans to find the right fit for you.

Privacy Secured | Advertising Disclosures

Banking Products

Find the right place for your money

Banking shouldn’t be a hassle. Compare the best savings accounts for your money.

Privacy Secured | Advertising Disclosures

Student Loans

Compare student loan options

Pay for school the smart way. We’ll help you shop and compare your options in minutes.

Privacy Secured | Advertising Disclosures

Find the right personal loan rate for you

Need to consolidate debt or make a large purchase? We bring the lenders to you so you can shop and compare personal loan offers in minutes.

Put your home’s equity to use

With home values higher than ever, now’s the time to make the most of your equity. Compare offers in minutes.

Compare top mortgage lenders

Get multiple lenders to compete for your business and see how much you could save. It pays to compare your options — literally.

Shop and compare credit cards

From earning rewards to transferring a balance, find the right credit card to help you score everyday wins.

Find the best insurance rates for you

Compare top insurance companies and get affordable, customized coverage for your car, home and more.

Shop and compare business loans

Our network of lenders will compete for your business, so you can get the funding you need for yours.

Where smart habits take root

Track your credit score, get personalized financial recommendations, and grow your credit health — all in LendingTree Spring. It’s free and available now!

Compare mortgage refinance offers

Get personalized refinance offers from multiple lenders in minutes and see how much you could save on your mortgage.

Compare debt relief options

It’s never too late to find relief. Stop juggling bills and resolve your debt with one simple monthly payment.

Discover the right auto loan for you

Take home the car you love. Compare auto loans to find the right fit for you.

Find the right place for your money

Banking shouldn’t be a hassle. Compare the best savings accounts for your money.

Compare student loan options

Pay for school the smart way. We’ll help you shop and compare your options in minutes.

Privacy Secured | Advertising Disclosures

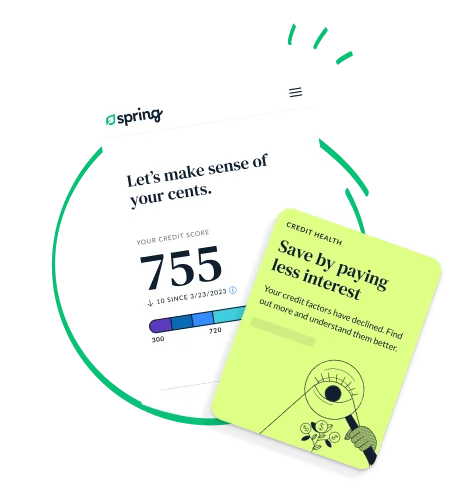

NEWIntroducing LendingTree Spring

Want to take control of your finances but not sure where to start? Spring helps you unlock a whole new world of potential, one easy step at a time.

Introducing LendingTree Spring

Want to take control of your finances but not sure where to start? Spring helps you unlock a whole new world of potential, one easy step at a time.

1

Security

Instead of sharing information with multiple lenders, fill out one simple, secure form in five minutes or less.

2

Savings

We'll match you with up to five lenders from our network of 300+ lenders who will call to compete for your business.

3

Support

We provide ongoing support with free credit monitoring, budgeting insights and personalized recommendations to help you save.

Mortgage

APR rates as low as

7.88%

5/1 ARM

$200,000 LOAN

Home Refinance

APR rates as low as

6.93%

30 year fixed

$200,000 LOAN

Personal Loans

APR rates as low as

6.99%

3 year

$20,000 LOAN

HELOC

APR rates as low as

6.99%

30 year fixed

$50,000 LOAN

Grow your financial confidence with a free Spring account:

Get Spring For FreeBest Credit Cards in April 2024

14 Best Rewards Credit Cards in April 2024Personal Loans

Bad Credit LoansBest Credit Cards in April 2024

Best Balance Transfer Credit Cards with No Transfer Fee in April 2024Personal Loans

When and How to Refinance a Personal LoanBest Credit Cards in April 2024

13% of Millennials are Debt-Free, Credit Card Debt Most Common ProblemLendingTree is a marketplace, built to save you money—we don't make loans, we find them. In fact, we've been finding the best loans for Americans for more than 20 years. Our marketplace is the largest in the country, and it's filled with lenders you know and trust.